Tracking your finances is a step most people skip when trying to make a budget or live frugally. Let me walk you through the simple process… and give you a free download to help you get started today!

If you’ve ever struggled to create a budget, or you’ve created numerous budgets but struggled to actually stick with them, it’s probably because you didn’t have an accurate picture of how much you make, save, and spend in any given month or year.

That’s where my simple Finance Tracking Workbook comes into play — think of it more as a pre-budgeting tool.

NOTE: My Finance Tracking Workbook is NOT a budget workbook.

I’m not here to help you lay out your specific budget for the year… but I will give you a tool that should eventually allow you to create a realistic budget for your current family and stage of life (if you want to create a budget)

If you don’t want to create a budget (we don’t) the Finance Tracking Workbook is still a really helpful tool that allows you to easily and instantly see exactly how much you’re spending in various categories on a monthly and yearly basis.

My Finance Tracking Workbook will not limit how much you can spend; it will simply tell you how much you already are spending.

My Finance Tracking Workbook will not prohibit or incentivize you to save, invest, or give… but it will tell you exactly how much you already save, invest, give, etc.

It’s nothing fancy (I’ve been using roughly the same system since I was 18 years old) but it has worked for our family for more than 2 decades and it has worked for thousands and thousands of you who have downloaded a version of this workbook since I first shared it back in 2011.

If you can commit to entering a few numbers into a Google Doc each week, you can do this!

Don’t Want to Budget? Track Your Finances Instead!

This finance tracking workbook is a great tool if you don’t want a budget.

Truthfully, we’ve never used a traditional “budget”.

Budgets have always felt too restrictive for me, as Dave and I are natural savers and don’t need to worry much about overspending.

As long as I keep tabs on how much we’re spending in certain categories, I can easily pinpoint where we could cut back if we had to, or notice less-than-ideal spending trends.

If you’re not gung-ho about budgeting, I’d still encourage you to try tracking your finances for a few months or a year. It might be eye-opening.

I know it’s been fun for us to look back over the years and see how we’ve increased spending in some categories (ahem, groceries) while cutting back in others (travel, entertainment). And also, how our income, investments, and giving have morphed over the years.

Want to Budget? Track Your Finances First!

That said, if you’d like to create a budget but just don’t know where to start or how much to realistically allocate for gas, groceries, restaurants, etc. this Finance Tracking Workbook is a great first step.

By tracking your finances for several months (better yet, do it for a whole year) you’ll quickly and easily see how much you actually spend in a variety of categories.

This will allow you to create a much more realistic budget based on your current spending (not some random percentage suggested in a book or article).

For example, if you set an arbitrary grocery budget of $500 a month… you might be frustrated, wondering why you can’t ever stick to your budget. However, if you first track your spending and realize your “normal” grocery spending is closer to $1000 a month, you can set a more realistic budget (maybe $800 a month) so you’ll have a better chance of succeeding and sticking with your budget!

Make sense?

Ok, let me show you the workbook!

When you open the workbook as a Google Doc, you’ll see a page of simple instructions, explaining how to save A COPY of the workbook to your own Google Drive (you will not be able to edit the original).

At the bottom of the workbook, you’ll see 7 additional tabs (or worksheets):

- Income

- Debt (reduction)

- Bills

- Expenses

- Giving

- Investments

- Summary

Once you save a copy of this workbook to your own Google Drive, you’ll have the freedom to change the names of each tab, move the tabs around, add new tabs, or even completely delete the tabs I’ve created.

In fact, you will be able to edit EVERYTHING in this workbook to make it super functional for your specific needs!

No strings attached, no email opt-in, no “red tape”.

Shocked? You’re welcome. 😊

NOTE: If you’d like more free content like this, I send a short email every Wednesday morning with tips to simplify and organize your home and life. Enter your email below and click “join now!”

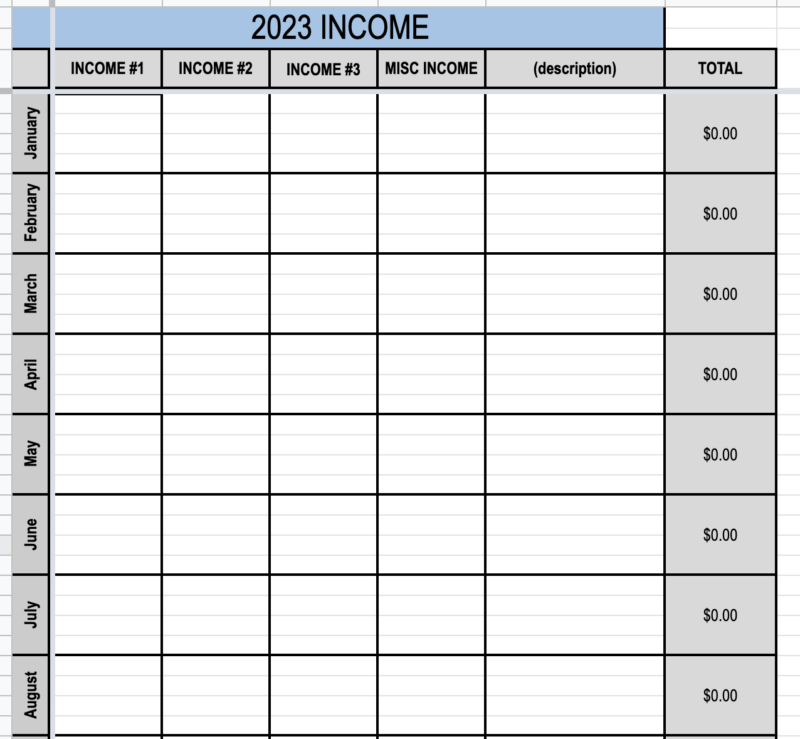

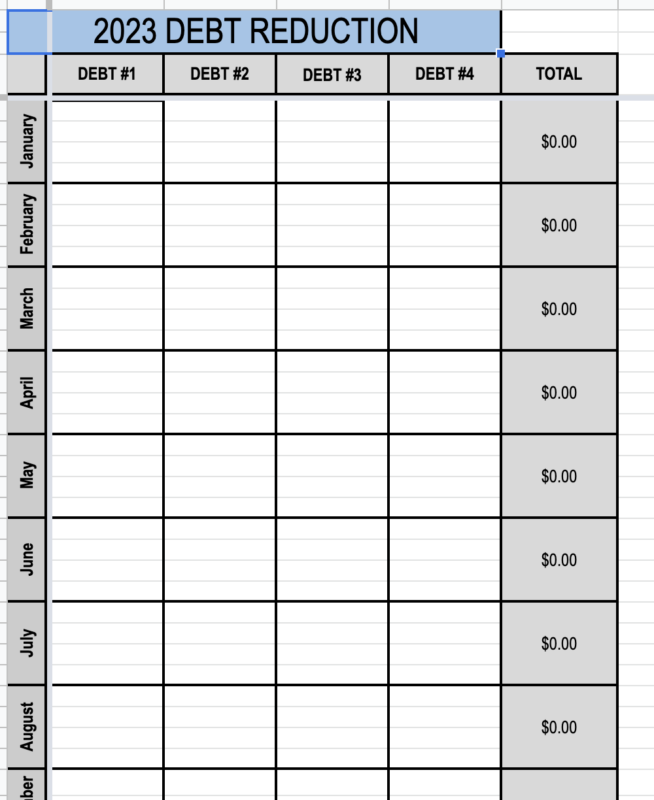

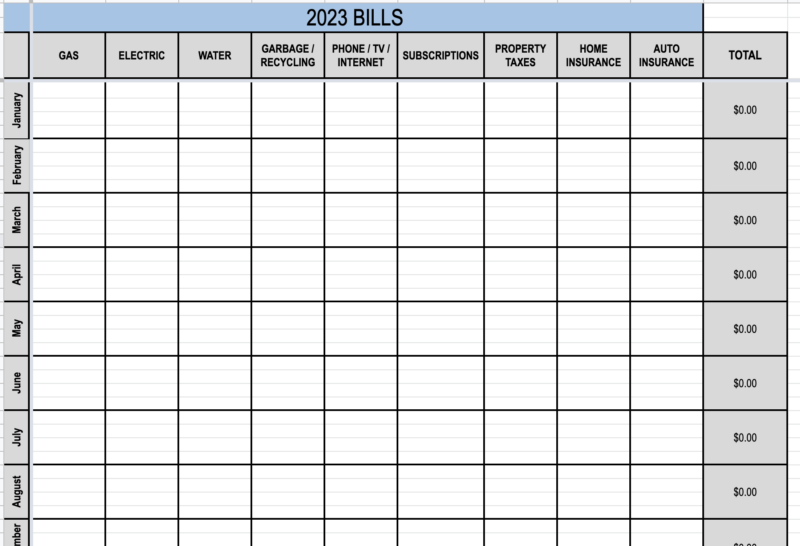

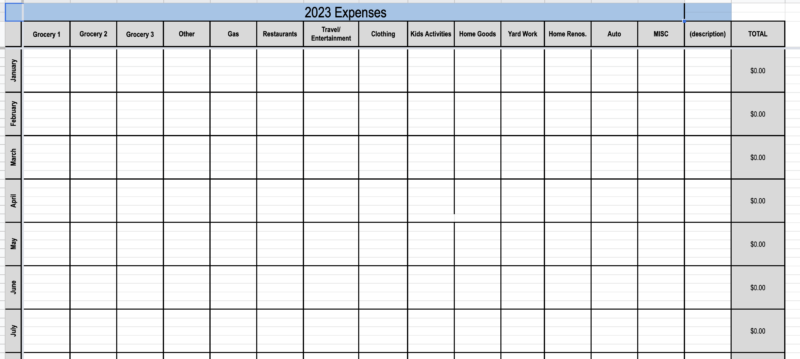

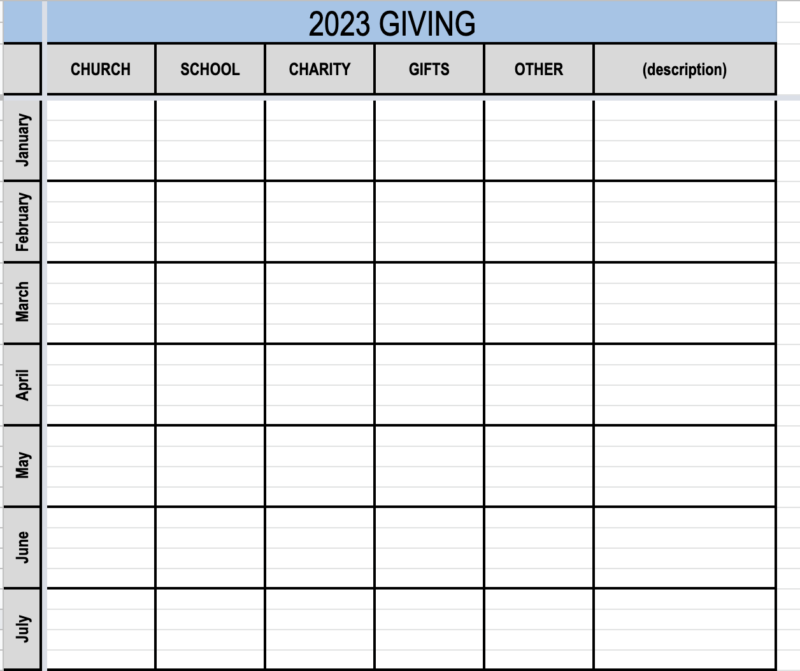

Within each tab/worksheet, I’ve broken the year into 12 months (see left column on photos below), and I’ve broken each month into 4 weeks (each row = one week), which makes it easy to track how much you make, spend, give, invest, etc. on a weekly, monthly, or yearly basis.

OK, let’s dive in…

1. INCOME:

Whether you want to create a budget or not, it’s crucial to know how much income you generate on a monthly and yearly basis. Without this information, it’s almost impossible to create an accurate budget.

And even if your goal isn’t to create a budget, it’s still important to know your average monthly income.

Use the INCOME worksheet to track all your various forms of income in one place (remember, you can change the names of the headings and add more columns if necessary).

2. Debt Reduction:

If you don’t have any debt, give yourself a pat on the back and delete this worksheet!

If you do have debt, the DEBT REDUCTION worksheet is the place to record how much you’re putting toward each debt on a monthly and yearly basis.

You can also record any extra, principle-only payments you make.

Related Reading: How we paid off our mortgage 24 years early.

3. BILLS:

Use the BILLS worksheet to track recurring expenses (natural gas, electricity, trash, cell phone, Netflix, car insurance, etc. )

Feel free to adjust the column headers to whatever works for your own “bills”.

I personally put different bill amounts in different rows — this is because each row represents one week, so if a bill is due on the 3rd week of the month, I put it in the 3rd row for that month. Or if the bill is only quarterly, I post it every 3 months.

4. EXPENSES:

In my opinion, expenses are different than bills.

I use the EXPENSES worksheet to track variable expenses such as:

- groceries

- gasoline

- restaurants

- clothing

- vacations

- home renovations

- kids activity fees

Again, you can adjust the column headers to be anything you want them to be.

The EXPENSES worksheet is the one I use the most often… partially because we have lots of small daily and weekly expenses to enter, but also because I like being able to quickly know how much we’ve spent in any given month or in any specific category.

It’s eye-opening to see the exact amount I’ve spent on groceries or clothing in any particular month or year. The numbers could indicate that we’re stewarding our resources well, or they could be a red flag that we need to be more intentional in certain areas.

Related Reading: Stop Money Leaks by Tracking Your Expenses

5. GIVING:

Quickly and easily track all your charitable giving and donations in the GIVING worksheet.

I have this worksheet set up to track multiple different donations (again, you can change this for your needs), and it’s always a bit of a game for me to see if we can surpass our percentage of giving each year (see “SUMMARY” page for the percentages).

This worksheet can be helpful as tax season rolls around too (all your charitable donations listed in one place).

And it’s a great way to monitor your spending during the holidays if you keep track of your “gifts” spending.

6. INVESTMENTS:

Even if you can only invest $10 a month, you should still do it!

I’m not an investment expert but we do pay someone to be our “investment expert” because we know how important it is to make wise choices with our money now.

I use this worksheet as a simple way to track our monthly investments.

Related Reading: How we automate our saving and investing.

Related Reading: How to start saving for retirement.

7. SUMMARY:

The SUMMARY worksheet is, well… the summary!

I have all the formulas set up so your totals from the previous six worksheets will automatically calculate and show up on the SUMMARY worksheet.

I love this at-a-glance snapshot of our finances at any given point during the year!

I’ve also added percentages to this sheet so you can instantly see what percentage of your income is going towards giving, bills, expenses, debt, and investments. This has been a fun stat for me to track over the years.

Note: The percentage values will show an error message until you actually record an income (see image below). Also, if you get error messages on the Summary page, it might be due to any changes you made on the other worksheets.

So that’s it — my simple system to track our savings and spending (say that 5 times fast!)

And it’s free, so you don’t have anything to lose by giving it a try. 🙂

When I enter information:

One of the most frequently asked questions I get about this workbook is:

How often / when do you enter your info on the spreadsheet?

In many ways, it has become somewhat of a daily thing for me — most evenings after the kids are in bed, I’ll open up the workbook and enter anything from that day.

It takes less than a minute.

Sometimes I go a few days if there’s not much to enter.

I have a spot right next to my computer where I save any receipts that need to be entered, and I have a “To Record” folder in Gmail where I save any digital receipts, income statements, or bills until they are recorded.

Again, it’s a super simple system, but it has worked for me from my poor college days through 2 moves, 4 children, and many years of running a business from home!

If you’re looking for an easy way to get a handle on your savings and spending, I hope my Finance Tracking Workbook will work for you. Please let me know if it does 🙂

Once you start tracking your income, expenses, bills, debt, etc., you’ll have a much better handle on your overall financial situation… which means that if/when you want to create a budget, you’ll be able to use “real data” and not just throw out arbitrary numbers.

And if you don’t want to take the next step of creating a budget, you can simply enjoy looking back over the years and comparing your saving and spending (or maybe I’m the only weird one who likes to do that!)

Open my FREE workbook, make a copy, save it to your own Google Docs or your computer, and start tracking your saving and spending!

Do you currently track (or have you ever tracked) your finances?

Lyndsey says

Thank you for this tracking sheet! We used excel for budgets in the past. I was able to make them look so pretty, but following them didn’t always work out the best. I LOVE the idea of tracking! Game changer for sure. Thank you for being a blessing to our family! I look forward to your Wednesday emails!

Andrea says

Yay — you’re very welcome! And yes, “tracking” is usually a lot easier than “budgeting”, especially in the beginning. You need to know how much you actually spend before you can create a strict budget 🙂

Enjoy!

Gloria says

Hi Andrea, I love the finance tracking workbook. I have been using it for about 3 years now. I am not a budget person, but I like seeing where my money is going each month, so I can get cut back in areas where I need too. I love how you can make it your own and replace the titles with what is going on in your life/household. Thank you

Andrea says

you’re welcome! So glad this has been working for you for a few years now already!

Nancy says

I am in love with the finance tracker! I used to use Quicken but then I got married. My (IT Security) husband doesn’t like all the banking and credit cards hooked into some program. And I am way too illiterate to develop these Excel things myself. Thank you so much!!!

Andrea says

you’re very welcome! Enjoy!

Sarah Spencer says

I’ve been using your finance tracker for 3 years (just started using it for our 4th year)! It has been SO helpful, Andrea! I kept trying to budget, but felt like a perpetual failure. After just a few months of committing to tracking – rather than budgeting – I was amazed at how it really helped us see where we need to cut back. It’s been so effective that it helped us curb expenses, pay off a MOUNTAIN of school debt, and buy a home with a large down payment last year! Thanks for all you do and for sharing practical tips year after year.

Andrea says

yay — Thanks so much for sharing your success with this simple workbook!

I’m thrilled it has been helpful for you and your family — and congrats on the debt payoff and the new house!

Rhonda says

I only do “big picture” budget on a simple Google Sheet. It includes income and *most* of our bills. Still, within that, I really only estimate what I *think* we spend on gas or groceries. I love the idea of this tracker and think it’s awesome that you created it and are willing to share with others! But in reality, it wouldn’t work well for us because although I could do it, it’s not likely that my spouse would. On the other hand, we are like you and Dave – naturally save a lot and don’t tend to overspend (if anything, I think I am an underbuyer!) I could see some people using this tool not to SAVE on their finances, but to actually to see if they could allow themselves to SPEND more (as in the “Die With Zero” concept/book) – perhaps more travel to see friends or relatives, fun experiences, etc.

Andrea says

yes, definitely! I think you would probably be in the minority if you’re using this workbook to help you spend more versus save more (but I totally understand where you are coming from!)

Janel says

Oh my goodness. I have needed something like this for so long and didn’t have the ability to get it all sorted into these much needed parts. I particularly love the summary page at the end. Oh my goodness- I’ve been needing some kind of resources to help me see the big picture of my finances.

Andrea says

great — glad to help you out Janel! I hope you enjoy the workbook this year!

Gloria says

I love this Finance Tracking Workbook but I am not computer savvy. Can someone tell me how I add more columns across and more lines down for each month. I am confused. Thank you

Andrea says

Hi Gloria, it might be easiest to “google” your question. Chances are a video tutorial will pop up and they’ll walk you through the process.

Betsy Gilberti says

Hi Andrea,

Thank you for sharing your file, so smart! I have been weirded out by the idea of using a percentage budget before seeing the footprint as single or a family, where you live, in a specific year, and then stressed by unrealistic guidelines or feeling like a failure for not meeting the demands. Your plan to view spending first has greater hope of a realistic approach to spending success.

Hoping to use this successfully in 2023. My concern is my need to continue being a dinosaur and using Excel. Other than dates, did you change anything else from the original Excel version if I would like to copy that one?

Andrea says

oh good — I’m thrilled my approach feels more realistic to you (that’s my goal!)

I did change a few things from the Excel version (like adding in the percentages) but it’s basically the same. If what you’re using currently works for you, then just keep using it!

Molly says

Thank you, thank you for sharing! Finance-wise, I think very similarly to you. I do have a question though..when entering bills, do you enter them in the month that you receive the bill, or do you enter them in the month you pay the bill? I receive some bills in the middle of the month, and then pay them at the beginning of the next month (before the due date). Does that make sense? Or do you pay them right on the due date? I’m scared to do this in case I forget:)

Andrea says

Hey Molly!

All our bills are set to auto-pay and charge directly to our credit card (which is then automatically deducted from our bank account every month)… so I don’t actually ever sit down to “pay the bills”. That said, when I get the payment receipt via email, I save it in my “to record” folder in Gmail and eventually enter it into my finance tracking spreadsheet in the week/month it was PAID.

Amanda says

Thanks for sharing this! I’m going to give it a whirl, starting this week! Wishing you and all the viewers a Happy New Year!

Andrea says

great! I’m thrilled for you (and your finances!)

Happy New Year, Amanda!

Rhonda says

Thanks Andrea. I’m going to give this a try. I’ve used your “Important Information Binder” template for a few years, and now I don’t even give it much thought (updating is so easy). I have my own simple “budget” spreadsheet, but I don’t really drill down with 100% real data. We’ll see if my arbitrary numbers match very close to the real numbers!

Andrea says

YES — once you have the documents created how you like them, it’s so quick and easy to update them. The hard part is just getting started!

Jamie Gottlieb says

My husband created a similar spreadsheet and fills it out for us. I am thankful he is so organized and tracks our spending. We have a yearly meeting in Jan. to look back and see what we need to adjust in terms of spending, investing, etc.

Andrea says

yay — so glad your hubby is so organized with your finances 🙂

Fran says

Wishing you and your family a very Merry Christmas and a wonderful New Year ❤️

Andrea says

Thanks so much Fran 🙂

Pat says

Love this!! What a great start!! The hardest part is to start and you made it sooo easy!! Thank you

Andrea says

The hardest part is ALWAYS getting started — I’m happy to make that just a bit easier for folks!

Kim Utz says

I have loved and used this tool for years now and have customized it for my needs. One thing I am wondering if it does that I just don’t know how to do is to capture the summary information by the month as well as the yearly running total? I hope that question makes sense!

Andrea says

yay — that’s fantastic news. I’m thrilled that you have personalized it and made it work for you and your family!

So… to do a summary by month, you’d need to set up a new worksheet and have 12 separate “summaries”. You could copy and paste the chart on my main “summary” worksheet, and then change the formula so it takes the total from the monthly rows instead of the total from the entire sheet.

Not exactly sure how to explain this — let me know if you have more questions (maybe just shoot me an email: an****@**********er.com)

Nancy says

Thank you so much! Merry Christmas!

Andrea says

you’re very welcome, Nancy!

Calliope says

LOL…If we were twins, it is unlikely that we’d be so…similar.

I fill in an almost identical excel file since I was a university student.

And I,too, do it every night before bed.

Super helpful for me, not so much for my husband though!

Andrea says

hahaha — so funny!

Glad you have your own spreadsheet that’s working well for you! 🙂

Angel says

Just what I was looking for after an exhausting search for the right forms, thank you thank you thank you

Andrea says

yay! Glad to help!